- 189

- 313

- Joined

- Feb 3, 2014

I make happiness and I save moments. Word to life.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

#HumbleBragJust graduated but I ran some quick numbers for when I start working in a month:

$65k salary

Roughly $4k a month after taxes

Plan on saving $2.4k in investments

Save whatever I don't spend from my food/spending budget

@ModernDarwin

woah 2600 for rent? Where do you live. If possible try to cut that down to atleast $2000 , personally I wouldn't pay more than $1200/mo on my mortgage/rent.

From what you are saying you wont have enough to pay all of those bills 5200 after tax will be close to 4000 or less after taxes. You can check out your exact paycheck on a site that calculates your paycheck with taxes and 401K factored in. Here is the link

#HumbleBrag

#ImHereToShowTheWorld

@INshoeKid You sound like you have it made. Hope you stick around the thread and help us learn from your successes. Where in the Midwest do you reside now?

af1 1982 Congrats on the graduation and that's a great starting salary! What was your major/what job did you get/where you located?

said it was the smart investment to do until I no longer qualify.

said it was the smart investment to do until I no longer qualify. lets get it

lets get itI got the saving part down, I need some advice on how to make my money work for me.

Got my money sitting around doing nothing

What locations will you be rotating to? I have a friend in a rotational program and his is already in a management position after only 1 year. The program has given him so much exposure that the CEO knows him by name. I am very interested in rotational programs due the exposure and fast track to executive positions.

My current employer and most govt contractors require a Masters to get into a rotational program, so I will try to get in as soon as I finish my MS.

timcity2000 I agree I use Mint to keep track of my budget and Personal Capital to keep track of my net worth and investments. Wish PC improved their budget features so I can drop Mint.

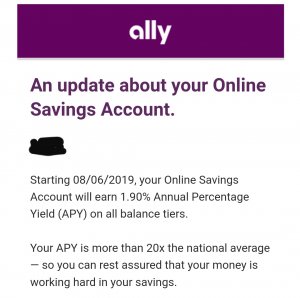

where do y'all park your emergency funds? mine is in a low-interest savings account at the moment... easy to get to obviously.

guessing there are smarter options?

I plan on putting my emergency fund in one of my savings for easy access. How much yall putting in there? I was thinking $5k

I plan on putting my emergency fund in one of my savings for easy access. How much yall putting in there? I was thinking $5k

"rules of thumb" are all over the place, but i typically see recommendations for 3-6 months of LIVING expenses (i.e. not 3-6 months of salary).

certainly depends on a number of factors... job security being a big one.