- 707

- 237

- Joined

- Aug 7, 2012

I can't seem to win in this forex market! FML

Last edited:

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

I hate this country....

I checked on paycheckcity I know I'd be putting a lot of OT in this year.

So I put out a number.. If I made about 100K this year, after taxes, Ill only be able to touch 60K

thats if I put nothing in any 401/457 plans. So its surely less after I put in my contributions.

Sucks being a single person trying to get their lives in order... You get taxed so heavily.

Common misconception is that you're "jumping" to and from tax brackets:So if I understand it right , if u put a lot into your 401k it reduces your FIT taxable and can put u into a lower tax bracket , potentially. Is that right? Maybe if u have enough deductions (home ownership) you'll get into that tax bracket if the 401k deductions didn't get it there

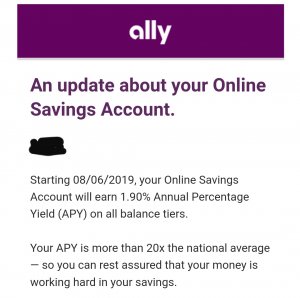

1.05% on your balance. The other percentages are on the interest you gained, not your balance.anyone open a barclay's dream savings account? 1.05 and 2.5 percent bonuses for depositing an amount monthly and another 2.5 percent for no withdrawals.

thanks in advance

Off the top, accounts like the PARS/PERS are deferred retirement accounts that public/government employees receive.

Don't know too much about IRA. Just looking into the stuff. I have a retirement account from an old employer, PARS to be exact. Was wondering should I open an IRA or is the account I already have good enough?

If someone is debt free except the mortgage, and makes good income, what takes priority- 401k or extra mortgage payments?

I'm thinking with my age (33) I want to put as much as I can into my 401k to take advantage of time x growth. Since the mortgage rate is fixed at a good rate, I'm going to try to max out my 401k first, then pay towards mortgage after the limit is hit for the year. Sound thinking?