- 12,038

- 14,850

- Joined

- Jul 27, 2013

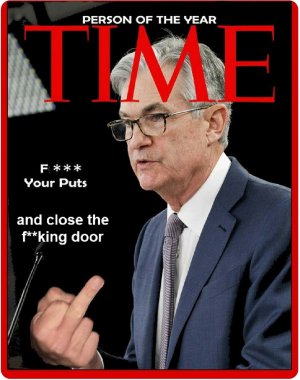

His “cash is trash” will go down as one of the worst calls in history.

I wonder how renaissance technologies is doing. My friends are begging me to manage their money for them, I jokingly said I want my 2/20% but I might raise that to 4/40% if I’m outperforming Simmons.

How about 2/25...where shall I wire funds??

.

.