- 1,391

- 1,024

- Joined

- May 24, 2013

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

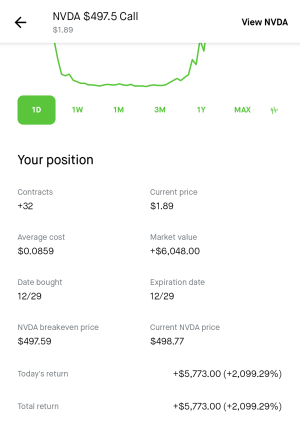

I’ll post a chart tomorrow but basically the last big pullback nvda had essentially a $100 down move from the highs. This one has been really struggling getting through supply and keeps getting stuffed into the 548 supply zone. When it clears through there and confirms finally it’s going to 600+ but for the time being 516 remains a downside pivot that needs to hold. We closed above it today so the hedge is premature but if that fails and we cascade, I do expect this stock to wash out another 80-100 bucks where the next VPOC (level of heavy volume traded at that price that hasn’t been touched) at 415 will be a potential downside target. Now this will only occur in a weak tape and I’m thinking we see a crack soon in the market but I could be very early. I’m only taking this hedge because the r/r is insane and it gives me some protection if the market which is very overbought corrects a little. Best thing we can see honestly is consolidation for two months and let moving averages catch up and valuations be worked off.There has to be a catalyst to this play that you’re not telling us about.

What throws me off is there isn’t a real investor presentation on their investors relations page which looks sus as hell. Having said that, get paid papi this could run.Weedmaps

Plus, it was a new concept at the time, so you have to get people on board. It was also going up against the norm of video rentals and on-demand rentals. Usually, the first man in takes the most bruises.Gotta take into account that most people didn’t have smartphones and computers 10+ years ago. Everyone today has something to watch Netflix on so ofcourse subscription count would grow exponentially on any new service. I still don’t know anyone that has a Disney+ account.

Only people i know are those with young kids. Everyones at home, kids are probably annoying the **** out of the parents so they throw on some Disney movie(s) to quiet them down.Gotta take into account that most people didn’t have smartphones and computers 10+ years ago. Everyone today has something to watch Netflix on so ofcourse subscription count would grow exponentially on any new service. I still don’t know anyone that has a Disney+ account.

HBO Max got the deal with Warner bros. They setting the tone already.When most movie theatres go away, Im curious to see what streaming service takes over.

Amazons gonna buy AMC. World domination continuesAmazon will make a statement if needed to dominate d2c releases

Amazons gonna buy AMC. World domination continues

Tesla prediction for this week before s&p500 inclusion?

How much liquidity do you have?

Dont get my hopes upI have no comment

About 37k

Dont get my hopes up

Never. Only thing letting me down these days is my horrible choice of sports teams.Have I let you down?

Never. Only thing letting me down these days is my horrible choice of sports teams.