- 70,049

- 24,221

- Joined

- Aug 1, 2004

Sean Gauthier looks through his sneaker collection, some of which he financed through installment payments. AMY LOMBARD FOR THE WALL STREET JOURNAL

FINANCE

Eyeing That Sweater? It’s Yours in Four Easy Payments

Fintech firms pitch installment plans to consumers increasingly reliant on borrowing

By

AnnaMaria Andriotis and

Peter Rudegeair

Sept. 28, 2019 8:00 am ET

Sean Gauthier wouldn’t think of using credit cards to buy sneakers.

“I try to save them for an emergency situation,” said Mr. Gauthier, a 38-year-old nightclub manager from New London, Conn. “If I start online shopping with my credit card, I’ll start getting nutty.”

But recently, while browsing a $140 pair of white, pink and green Nikes on the app of footwear retailer StockX, he tapped on an offer from financial-technology upstart Affirm Inc. that let him buy the shoes right away and pay for them over six months. He could have bought the colorful kicks outright, but Mr. Gauthier, who has used Affirm several times, said the $5 the company charged him in total interest was a small price for flexibility to pay over time.

Gone are the days when special financing plans were mostly reserved for big-ticket purchases like TVs and refrigerators. Now, sweaters, makeup or other everyday items can be paid for in installments with loans or other payment plans offered at checkout with thousands of merchants in the U.S., including Walmart Inc., Urban Outfitters Inc. and, soon, H&M . Some Amazon.com Inc. credit-card users can also sign up for these plans.

SHARE YOUR THOUGHTS

Would you choose an installment plan over a credit card? Why or why not? Join the conversation below.

Merchants and lenders are tapping into the financial challenges many U.S. families are facing. Despite signs of a strong economy, like low unemployment, consumers are increasingly relying on borrowing to fund their daily lives. U.S. consumer debt is higher than ever, as cars, college, housing and medical care grow more expensive but incomes stay largely stagnant.

The payment plans often resonate with young adults who are wary of carrying credit-card balances after watching their parents struggle with debt during the last recession. Fintech companies such as Affirm, Afterpay Touch Group Ltd. and PayPal Holdings Inc. dove into these payment plans after that period, when banks pulled back on consumer lending.

Growth is booming. Affirm’s point-of-sale loans doubled to about $2 billion last year and are expected to at least double again this year, CEO Max Levchin said.

Reliable, industry-wide statistics about the size of this market are hard to come by, and it is tiny compared with the roughly $450 billion of spending limits on new U.S. credit cards that Experian PLC says were issued last year.

But more than half of merchants surveyed this year by advisory firm 451 Research said they already offered installment options or planned to adopt them in the next year. Nearly 40% of consumers surveyed said the ability to finance a purchase at checkout made it more likely they would complete a transaction.

Big financial firms, eager to expand their consumer lending, are getting in. JPMorgan Chase & Co., Citigroup Inc. and American Express Co. have introduced or are working on payment programs for cardholders that resemble installment loans.

Sean Gauthier’s sneaker collection, financed through the fintech company Affirm, include (from left) a pair of Nike Air Max 90, Reebok Shaq Attaq All-Star and Reebok Shaq Attaq Packer shoes. PHOTO: AMY LOMBARD FOR THE WALL STREET JOURNAL

Some consumers, like Mr. Gauthier, have credit cards but prefer the structure of point-of-sale loans. Interest rates are often lower. The loans last for only a set, relatively short time. And borrowers also generally know up front how much they’re going to pay in total.

Say a borrower buys a $100 outfit. With a credit card, he will need to pay that off by the next due date or carry a card balance, which can last months if he makes only the minimum payments and racks up interest charges. With an installment loan, he pays a fixed amount with each payment—say, $25 each month over the following four months, or more depending on interest or other charges—and knows ahead of time what the total will be.

In some ways the offerings echo layaway plans that were popular in years past, though in those cases the buyer didn’t usually get their item until after they’d made all their payments.

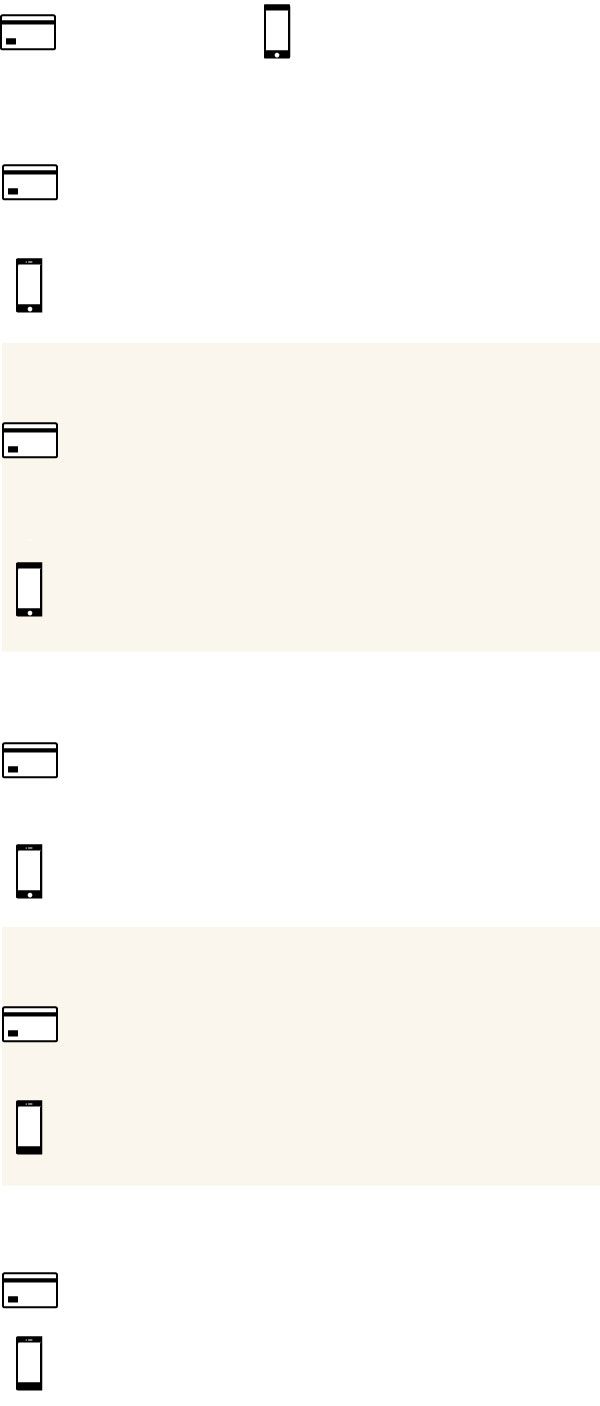

New Credit

What are the differences between a traditional credit card and an Affirm loan?

Credit card

Affirm

How does it work?

The debt is wrapped into what you owe from other card purchases.

The debt is for a specific purchase.

How do I repay it?

A minimum payment is due monthly and late fees are often added if you miss a payment.

The payments are broken into equal monthly installment plans.

How much interest do I pay?

Interest is applied to your balance. Interest charges can change.

Interest charges are specified up front.

How long does the loan last?

Until you pay it off. There is no predetermined end date.

Your payment schedule has a fixed end date.

Where can I use it?

Most stores.

Mostly online retailers that have partnered with Affirm.

Some borrowers say the installment plans force them to be more disciplined about paying back the money, and that they feel like they have more control since they’re borrowing for a specific item.

“When you put something on a credit card, it vanishes into a big black ball of debt,” said Guy Stephens, of Lusby, Md., who has paid for a vacation and mattress using Affirm. “There are balances I’ve had over time where I don’t even know what I bought.”

Larger purchases can require relatively big monthly payments. For example, a borrower who makes a $400 purchase might have to pay it back in four $100 installments. With a credit card, the minimum required payment each month would likely be much smaller.

These plans are generally offered to customers while they are browsing products or about to purchase an item, often online but sometimes in stores as well. Retailers hope such services will draw in new customers and prompt them to spend more. The fintech companies typically collect money from merchants for each sale.

Like credit cards, the loans are unsecured, which means lenders generally can’t repossess particular items if borrowers fall behind on payments. Borrowers can be referred to debt collectors.

Some borrowers use the installment loans because they don’t qualify for a credit card. Some of the companies providing the loans review non-traditional data about borrowers. For example, Affirm at times reviews applicants’ bank account balances.

Heidi Peyser said she was rejected for several credit cards after she fell behind on bills. While shopping for a mattress on Purple.com, she saw Affirm’s option that allowed stretching the payment over six months. “I thought ‘Well, let’s see how this goes,’ ” she said.

Ms. Peyser, a 39-year-old web designer in Santa Rosa, Calif., has signed up for five Affirm financing plans since 2017 to buy woodworking tools, a gel to help with joint aches and other items. She recently paid off the loans.

Some installment options don’t charge interest. Afterpay allows shoppers to divide purchases into four payments that are typically deducted from the customer’s debit card. Though it doesn’t charge interest, it does assess late fees for missed payments. The Australia-based fintech company has partnered with more than 6,500 U.S. merchants since entering the U.S. market last year.

Erica Padilla has used Afterpay plans to buy clothes for herself and her three children, including items from Baby Teith (left), Kervology (top right) and Nasty Gal. PHOTO: JEREMY M. LANGE FOR THE WALL STREET JOURNAL

Erica Padilla, 37, of Charlotte, N.C., has signed up for 19 Afterpay plans since last year. Ms. Padilla, a stay-at-home mom, tries to make her purchase due dates coincide with her husband’s paydays: “It makes it easier to think, ‘OK, I have to pay $25 now’ [rather] than spending $100” upfront, she says.

For Christmas, Ms. Padilla used Afterpay to buy $75 of videogame T-shirts for her 13-year-old son at Forever 21 and $60 of rock-themed tops for her toddlers. Without Afterpay, she said, “we would have definitely bought less.” She has since paid off those balances.

RELATED STORIES

Card companies have also been expanding their presence in the sector. Mastercard Inc. this year purchased Vyze, a technology company that enables point-of-sale lending. Citigroup and AmEx let customers convert some of their card purchases into installment loans, and JPMorgan will soon introduce that. Visa Inc. in June announced that U.S. banks that issue Visa cards will be able to offer installment options.

Catherine Tabor, 24, has used the AmEx arrangement nine times since late last year, including for Fleetwood Mac concert tickets and an opera house tour.

Ms. Tabor, who goes to law school in Tuscaloosa, Ala., and is working part time, has paid off those balances.

"I’m not making a whole lot of money,” she said, “so this is really helpful.”

Erica Padilla, photographed at her Charlotte, N.C., home, has signed up for 19 Afterpay payment plans since last year. PHOTO: JEREMY M. LANGE FOR THE WALL STREET JOURNAL

https://www.wsj.com/articles/eyeing-that-sweater-its-yours-in-four-easy-payments-11569672000

FINANCE

Eyeing That Sweater? It’s Yours in Four Easy Payments

Fintech firms pitch installment plans to consumers increasingly reliant on borrowing

By

AnnaMaria Andriotis and

Peter Rudegeair

Sept. 28, 2019 8:00 am ET

SHARE

TEXT

62 RESPONSES

Sean Gauthier wouldn’t think of using credit cards to buy sneakers.

“I try to save them for an emergency situation,” said Mr. Gauthier, a 38-year-old nightclub manager from New London, Conn. “If I start online shopping with my credit card, I’ll start getting nutty.”

But recently, while browsing a $140 pair of white, pink and green Nikes on the app of footwear retailer StockX, he tapped on an offer from financial-technology upstart Affirm Inc. that let him buy the shoes right away and pay for them over six months. He could have bought the colorful kicks outright, but Mr. Gauthier, who has used Affirm several times, said the $5 the company charged him in total interest was a small price for flexibility to pay over time.

Gone are the days when special financing plans were mostly reserved for big-ticket purchases like TVs and refrigerators. Now, sweaters, makeup or other everyday items can be paid for in installments with loans or other payment plans offered at checkout with thousands of merchants in the U.S., including Walmart Inc., Urban Outfitters Inc. and, soon, H&M . Some Amazon.com Inc. credit-card users can also sign up for these plans.

SHARE YOUR THOUGHTS

Would you choose an installment plan over a credit card? Why or why not? Join the conversation below.

Merchants and lenders are tapping into the financial challenges many U.S. families are facing. Despite signs of a strong economy, like low unemployment, consumers are increasingly relying on borrowing to fund their daily lives. U.S. consumer debt is higher than ever, as cars, college, housing and medical care grow more expensive but incomes stay largely stagnant.

The payment plans often resonate with young adults who are wary of carrying credit-card balances after watching their parents struggle with debt during the last recession. Fintech companies such as Affirm, Afterpay Touch Group Ltd. and PayPal Holdings Inc. dove into these payment plans after that period, when banks pulled back on consumer lending.

Growth is booming. Affirm’s point-of-sale loans doubled to about $2 billion last year and are expected to at least double again this year, CEO Max Levchin said.

Reliable, industry-wide statistics about the size of this market are hard to come by, and it is tiny compared with the roughly $450 billion of spending limits on new U.S. credit cards that Experian PLC says were issued last year.

But more than half of merchants surveyed this year by advisory firm 451 Research said they already offered installment options or planned to adopt them in the next year. Nearly 40% of consumers surveyed said the ability to finance a purchase at checkout made it more likely they would complete a transaction.

Big financial firms, eager to expand their consumer lending, are getting in. JPMorgan Chase & Co., Citigroup Inc. and American Express Co. have introduced or are working on payment programs for cardholders that resemble installment loans.

Sean Gauthier’s sneaker collection, financed through the fintech company Affirm, include (from left) a pair of Nike Air Max 90, Reebok Shaq Attaq All-Star and Reebok Shaq Attaq Packer shoes. PHOTO: AMY LOMBARD FOR THE WALL STREET JOURNAL

Some consumers, like Mr. Gauthier, have credit cards but prefer the structure of point-of-sale loans. Interest rates are often lower. The loans last for only a set, relatively short time. And borrowers also generally know up front how much they’re going to pay in total.

Say a borrower buys a $100 outfit. With a credit card, he will need to pay that off by the next due date or carry a card balance, which can last months if he makes only the minimum payments and racks up interest charges. With an installment loan, he pays a fixed amount with each payment—say, $25 each month over the following four months, or more depending on interest or other charges—and knows ahead of time what the total will be.

In some ways the offerings echo layaway plans that were popular in years past, though in those cases the buyer didn’t usually get their item until after they’d made all their payments.

New Credit

What are the differences between a traditional credit card and an Affirm loan?

Credit card

Affirm

How does it work?

The debt is wrapped into what you owe from other card purchases.

The debt is for a specific purchase.

How do I repay it?

A minimum payment is due monthly and late fees are often added if you miss a payment.

The payments are broken into equal monthly installment plans.

How much interest do I pay?

Interest is applied to your balance. Interest charges can change.

Interest charges are specified up front.

How long does the loan last?

Until you pay it off. There is no predetermined end date.

Your payment schedule has a fixed end date.

Where can I use it?

Most stores.

Mostly online retailers that have partnered with Affirm.

Some borrowers say the installment plans force them to be more disciplined about paying back the money, and that they feel like they have more control since they’re borrowing for a specific item.

“When you put something on a credit card, it vanishes into a big black ball of debt,” said Guy Stephens, of Lusby, Md., who has paid for a vacation and mattress using Affirm. “There are balances I’ve had over time where I don’t even know what I bought.”

Larger purchases can require relatively big monthly payments. For example, a borrower who makes a $400 purchase might have to pay it back in four $100 installments. With a credit card, the minimum required payment each month would likely be much smaller.

These plans are generally offered to customers while they are browsing products or about to purchase an item, often online but sometimes in stores as well. Retailers hope such services will draw in new customers and prompt them to spend more. The fintech companies typically collect money from merchants for each sale.

Like credit cards, the loans are unsecured, which means lenders generally can’t repossess particular items if borrowers fall behind on payments. Borrowers can be referred to debt collectors.

Some borrowers use the installment loans because they don’t qualify for a credit card. Some of the companies providing the loans review non-traditional data about borrowers. For example, Affirm at times reviews applicants’ bank account balances.

Heidi Peyser said she was rejected for several credit cards after she fell behind on bills. While shopping for a mattress on Purple.com, she saw Affirm’s option that allowed stretching the payment over six months. “I thought ‘Well, let’s see how this goes,’ ” she said.

Ms. Peyser, a 39-year-old web designer in Santa Rosa, Calif., has signed up for five Affirm financing plans since 2017 to buy woodworking tools, a gel to help with joint aches and other items. She recently paid off the loans.

Some installment options don’t charge interest. Afterpay allows shoppers to divide purchases into four payments that are typically deducted from the customer’s debit card. Though it doesn’t charge interest, it does assess late fees for missed payments. The Australia-based fintech company has partnered with more than 6,500 U.S. merchants since entering the U.S. market last year.

Erica Padilla has used Afterpay plans to buy clothes for herself and her three children, including items from Baby Teith (left), Kervology (top right) and Nasty Gal. PHOTO: JEREMY M. LANGE FOR THE WALL STREET JOURNAL

Erica Padilla, 37, of Charlotte, N.C., has signed up for 19 Afterpay plans since last year. Ms. Padilla, a stay-at-home mom, tries to make her purchase due dates coincide with her husband’s paydays: “It makes it easier to think, ‘OK, I have to pay $25 now’ [rather] than spending $100” upfront, she says.

For Christmas, Ms. Padilla used Afterpay to buy $75 of videogame T-shirts for her 13-year-old son at Forever 21 and $60 of rock-themed tops for her toddlers. Without Afterpay, she said, “we would have definitely bought less.” She has since paid off those balances.

RELATED STORIES

- Families Go Deep in Debt to Stay in the Middle Class

- Need Cash? Companies Are Considering Magazine Subscriptions and Phone Bills When Making Loans

Card companies have also been expanding their presence in the sector. Mastercard Inc. this year purchased Vyze, a technology company that enables point-of-sale lending. Citigroup and AmEx let customers convert some of their card purchases into installment loans, and JPMorgan will soon introduce that. Visa Inc. in June announced that U.S. banks that issue Visa cards will be able to offer installment options.

Catherine Tabor, 24, has used the AmEx arrangement nine times since late last year, including for Fleetwood Mac concert tickets and an opera house tour.

Ms. Tabor, who goes to law school in Tuscaloosa, Ala., and is working part time, has paid off those balances.

"I’m not making a whole lot of money,” she said, “so this is really helpful.”

Erica Padilla, photographed at her Charlotte, N.C., home, has signed up for 19 Afterpay payment plans since last year. PHOTO: JEREMY M. LANGE FOR THE WALL STREET JOURNAL

https://www.wsj.com/articles/eyeing-that-sweater-its-yours-in-four-easy-payments-11569672000