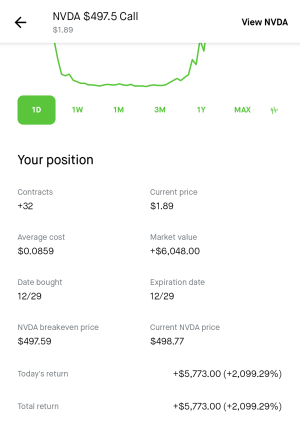

- 29,631

- 20,891

- Joined

- Dec 23, 2009

look at this ****ing bum. "They hate us cause they ain't us" defense. Opened a NKLA put a couple hours ago, $30 strike 10/02 exp, at $2. Up 16% after this stall defense.

look at this ****ing bum. "They hate us cause they ain't us" defense. Opened a NKLA put a couple hours ago, $30 strike 10/02 exp, at $2. Up 16% after this stall defense.Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

look at this ****ing bum. "They hate us cause they ain't us" defense. Opened a NKLA put a couple hours ago, $30 strike 10/02 exp, at $2. Up 16% after this stall defense.

Becky with the goodsPTON with insane numbers and guidance. Should be trading between $100-$150 if the market let’s it. Congrats.

Becky doesnt want to be forced to work out with Kyle's and Chad's every day. Cheaper bikes and new products make it more reasonable to buy. Online classes give the community feel of classes at gyms, without Karen's judging them.Someone that’s a pton bull sell me on being a buyer for sustained growth and not a covid anomaly. Numbers were great but is the TAM big enough to warrant the valuation and expected growth rate? Subscriber growth was great but still small numbers in the big picture.

Becky doesnt want to be forced to work out with Kyle's and Chad's every day. Cheaper bikes and new products make it more reasonable to buy. Online classes give the community feel of classes at gyms, without Karen's judging them.

The way I see it there is still a lot of untapped potential in the rental markets that are unaccounted for. Take myself for example: an avid pton user. I do not own but rather use one at my apartment. In the beginning, Pton was very agressive in partnering with apartments.. Pton has since moved away from the partnering with "luxury" apartment model to focus solely on the consumer market (I disagree, but see why) never the less they still have units in thousands of apartments across the U.S.....I fully intend on purchasing one when/if I buy my own place but without the need to yet, I continue to use my apartment subscription.Someone that’s a pton bull sell me on being a buyer for sustained growth and not a covid anomaly. Numbers were great but is the TAM big enough to warrant the valuation and expected growth rate? Subscriber growth was great but still small numbers in the big picture.

Yep. My options bets are going to die tomorrow. Only hope now is the earnings call having some additional news or extra guidance. ****, CHWY won but the market makers won bigger.Chewy beat but is down aftermarkets....

Shares of Chewy (NYSE:CHWY) decreased 1.41% in after-market trading after the company reported Q2 results.

Quarterly Results

Earnings per share rose 61.90% over the past year to ($0.0, which beat the estimate of ($0.16).

Revenue of $1,700,000,000 higher by 47.31% year over year, which beat the estimate of $1,690,000,000.

I've spent plenty of time in PA and San Mateo - we're looking north! Contemplating Washington but would still cover the Bay.

We’ve been there. I got shaken out of zm at 240 during the July volatility. Can always jump back in if the trend changes in your favor (exactly what I should’ve done with zm sooner). This eps and revenue growth for pton is pretty stellar. I think this could be sustainable potentially. Maybe they issue some stock to raise extra cash?Wouldnt have been much profit, but damn I really played this one terribly. I follow my sell rules too much sometimes.

Yeah we live in Seattle -I swear everyone from the bay is coming up - no state income tax is fantastic