- 26,254

- 3,387

- Joined

- Mar 29, 2008

cant wait to see how PINS does on earnings this week

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

Multi-TRILLION dollar market? Is there a company monopolizing oxygen?I had a day trade in CURI but sold it for a .30 scalp. Oh wells.

CML Pro members, at 8:30am PT we will release a new Spotlight Top Pick.

-

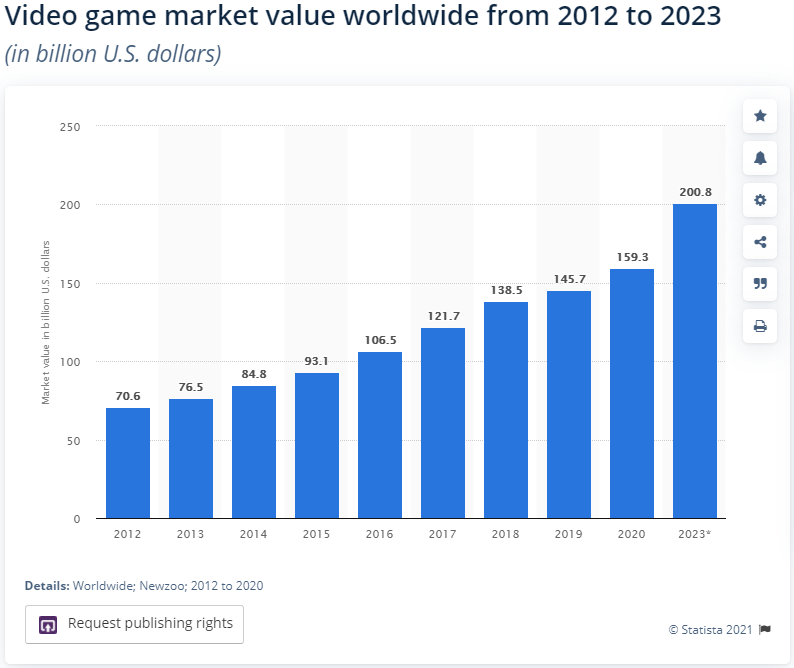

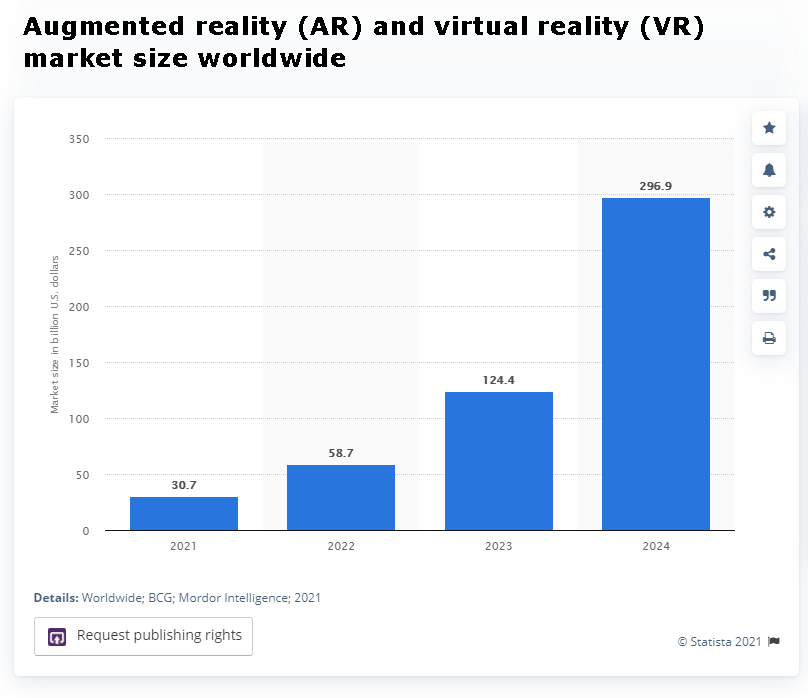

This may be the largest thematic we cover - a multi trillion dollar TAM.

The thematic is early, and non-obvious, and therefore finding companies that will drive it forward will take effort.

We like that version of the world. That’s our alpha.

This is our multi trillion dollar thematic and we will focus anew on opportunities with in it.

This is just one company. We will do our best to find more.

No no, please get into those reasonsA multi trillion TAM sounds like a supervillain has taken the world's water supply hostage.

Oh.... Well I can't buy that for reasons I cannot get into. Good luck!

What’s up with cciv today?

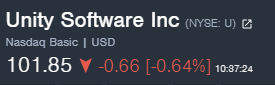

When I saw his post about TAM I pulled up U and saw the volume spike around 1030/11 and had a feeling. I bought more around 104. 7.4% position for me but I exited SQ to pay for the add and to buy more bitcoin. Trimmed nvta down to 1.8% to buy more bitcoin as well.johnnyredstorm did u see the pick ? damn u were in this already